The Research and Development Tax Incentive (R&DTI) has been modified with effect from 1 July 2021.

Entities will need to familiarise themselves with the new tax rules to ensure they have the best chance of qualifying for the incentive. At the same time, the accounting consequences should not be overlooked to ensure that the R&DTI has been appropriately dealt with in the financial statements.

Many businesses undertake some form of research and development (R&D) at a point in their lifecycle to build a competitive advantage over their competitors or to develop new or innovative products or services. R&D can be risky business as there is no guarantee that the product can be engineered or designed, or that fickle consumers will want the product.

The R&DTI is designed to encourage businesses to take the risk and try to engineer or develop new products, devices, processes, materials and the like.

While the R&DTI has been in effect since 1 July 2011, the federal government announced enhanced reforms to the scheme as part of the 2020-21 budget, acknowledging that investment in R&D is essential to help stimulate Australia’s economy. These enhanced reforms apply to income years commencing on or after 1 July 2021.

In this article, we cover a few of the key elements of the revised R&DTI regime before considering the accounting consequences.

Tax summary

One of the criteria to qualify for the R&DTI is that eligible R&D expenditure must be at least $20,000 for the income year concerned (if R&D expenditure is less than $20,000 entities can still claim the tax offset by using a registered Research Service Providor, or RSP, to conduct R&D). Under the mechanics of the scheme, relief is provided to eligible entities via a tax offset against the basic income tax liability, rather than via a tax deduction at the prevailing corporate tax rate.

For income years beginning on or after 1 July 2021, the tax offset is determined based on the amount incurred on eligible R&D activities undertaken during the income year as follows:

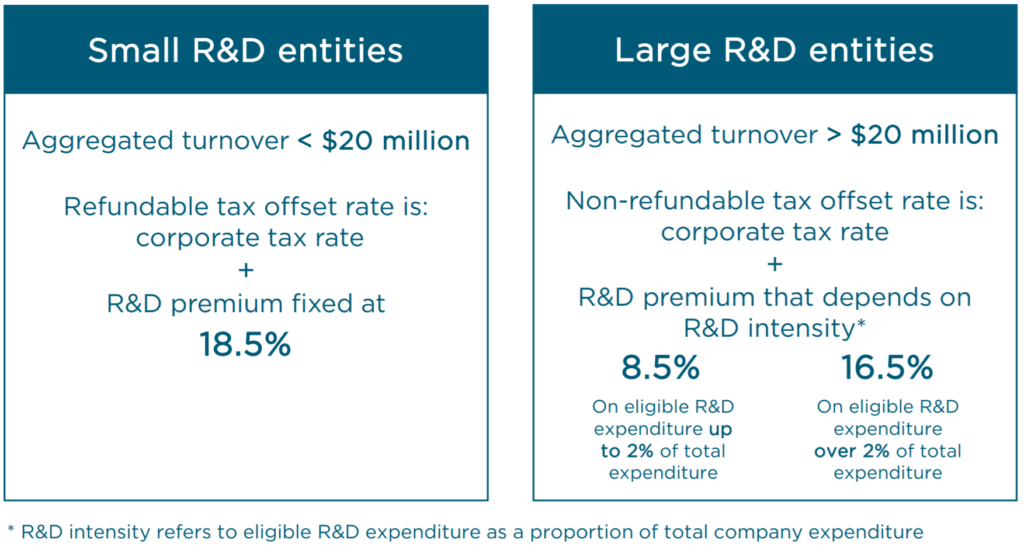

- For R&D entities with aggregated turnover of less than $20 million (‘small R&D entities’), a refundable R&D tax offset is pegged at a premium of 18.5% over the prevailing corporate tax rate. Therefore, a small R&D entity (which will also be a base rate entity), will be subject to a corporate tax rate of 25% for the 30 June 2022 tax year meaning the R&D tax offset will be 43.5%.

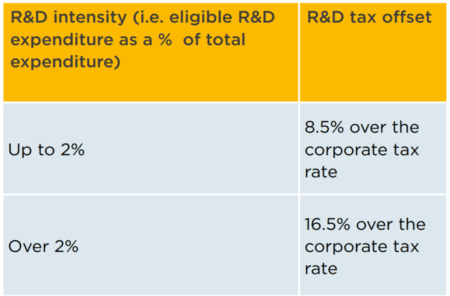

- For R&D entities with aggregated turnover of more than $20 million (‘large R&D entities’), a non-refundable R&D tax offset is the corporate tax rate plus a premium that increments based on the entity’s R&D ‘intensity’. The R&D intensity is broadly measured as the entity’s eligible R&D expenditure as a proportion of total expenditure for the year. There are two premium increments as follows:

With effect from 1 July 2021, a maximum threshold of $150 million per year applies to eligible R&D expenditure (this was increased from $100 million). This means that the R&D premiums over and above the corporate tax rate as detailed above can only be applied to eligible expenditure up to a maximum of $150 million. Any amounts above this cap are subject to an R&D tax offset equal to the entity’s corporate tax rate.

The refundable R&D tax incentive is refundable in cash to the extent that it exceeds the current income tax liability. The non-refundable R&D tax incentive, on the other hand, is applied against the tax liability with any excess carried forward to future years.

Accounting considerations

Which accounting standard applies?

The R&D tax offset is widely considered to be an ‘investment tax credit’ (ITC) as it relates to tax credits generated by eligible expenditure on R&D activities. The accounting for ITCs is, however, not specifically addressed in Australian Accounting Standards. This is because:

- AASB 112 Income Taxes specifically excludes from its scope the accounting treatment of ITCs (although the treatment of temporary differences arising from ITCs are within the scope of this

standard); and - AASB 120 Accounting for Government Grants and Disclosure of Government Assistance scopes out government assistance that is provided in the form of benefits that are available in determining profit or loss or are determined or limited based on the income tax liability, which includes ITCs.

In the absence of an Australian Accounting Standard that specifically applies to ITCs, it is a matter of judgement under AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors to develop and apply, on a consistent basis, the most appropriate accounting policy for the accounting treatment of ITCs.

AASB 108 provides guidance on the sources an entity must consider when developing an accounting policy, citing the first and most relevant source as being the requirements of Australian Accounting Standards dealing with similar and related issues. Despite ITCs being specifically scoped out of both AASB 112 and AASB 120, it is our view that these two standards are the most relevant standards to consider when developing an accounting policy for R&DTIs.

Refundable R&D tax offset

As mentioned above, the refundable R&D tax offset is first used to reduce the amount of any income tax payable by the entity. Any excess is then refunded in cash to the claiming entity.

A refundable R&D tax offset is analogous to a government grant as its purpose is to incentivise entities to invest in eligible R&D activities. That is, the R&DTI received by an entity is effectively a transfer of resources to an entity from the government in return for the entity engaging in and spending money on eligible R&D activities.

A government grant is defined in AASB 120 as assistance by government in the form of transfers of resources to an entity in return for past or future compliance with certain conditions relating to the operating activities of the entity.

On this basis, it is appropriate to draw guidance from AASB 120 to account for refundable R&DTIs. Consequently, where the R&D expenditure is not capitalised, the R&DTI is recognised as a credit in profit or loss (as part of earnings before interest and tax, or EBIT) rather than as part of income tax expense.

The corresponding debit will ultimately:

- reduce tax payable to the extent the entity has a tax liability sufficient to absorb the R&DTI; and/or

- increase cash (for any refund) to the extent the tax liability is insufficient to utilise the R&DTI.

In terms of presentation, R&D tax offsets that relate to R&D expenses that have been expensed (and not capitalised) are recognised in profit or loss, either as income or as a deduction from the related expense.

In the case where the related R&D expenditure is capitalised, the R&D tax offset is deferred (as deferred income) and amortised to profit or loss as the associated R&D asset is depreciated. Alternatively, the R&DTI can be offset against the carrying amount of the related R&D asset, thereby directly reducing the depreciation charge recognised in profit or loss.

When eligible R&D expenditure is capitalised under AASB 138 Intangible Assets, no deferred tax liability is recognised on initial recognition of the asset. The R&D asset has no tax base since the capitalised R&D expenditure is not deductible for tax purposes either at initial recognition or as it is depreciated. Also, the R&D tax offset is treated as a government grant, so no amount is recognised in determining taxable income nor is any amount recognised in profit or loss on initial recognition of the R&D asset. Consequently, the initial recognition exemption in AASB 112 applies and no deferred tax is recognised.

Non-refundable R&D tax offset

AASB 112 approach

The non-refundable R&DTI is available to entities with annual turnover exceeding $20 million. Where a non-refundable R&D tax offset exceeds the income tax liability, the excess is not refunded to the entity. Rather, the excess is carried forward and can be used in subsequent years.

As the non-refundable R&DTI is only available as a reduction in an entity’s current or future tax liability, many entities view this as being more akin to an income tax and therefore apply AASB 112 by analogy.

Under this approach, a credit is recognised in current tax expense to reflect the benefit of the R&D tax offset for each income year, with a corresponding reduction (debit) to the current tax liability.

For eligible R&D expenditure that is capitalised as an R&D asset for accounting purposes, the entity will recognise a deferred tax liability in respect of the capitalised amount. This will give rise to a deferred tax expense, offsetting the current tax benefit arising in the year the expenditure is incurred for tax purposes. The deferred tax liability will then reverse through deferred tax expense as the R&D asset is depreciated for accounting purposes.

The R&D tax offset is carried forward separately from carried forward tax losses and represents a tax offset to be used in future periods. As a result, the carried forward R&D tax offset behaves in the same way as an unused tax credit under AASB 112. Where an entity has carried forward R&D tax offsets, a deferred tax asset will be recognised which will be subject to the normal recognition criteria for deferred tax assets arising from unused tax losses and unused tax credits under AASB 112. This means a deferred tax asset can only be recognised to the extent that future taxable profits will be available against which the unused tax losses and unused tax credits can be utilised.

Other approaches

While the income tax approach discussed above is widely used to account for non-refundable R&DTIs, it is worth mentioning that there is diversity in practice due to the absence of specific accounting guidance.

Some entities treat the non-refundable R&D tax offset as a government grant, applying the principles of AASB 120, as discussed above.

Another less common approach is to use a combination of the income tax approach and government grant approach. Under this ‘split accounting’ approach, the portion of the nonrefundable R&D tax offset that is equal to the entity’s corporate tax rate (e.g. 30%) is accounted for by applying AASB 112 by analogy. The incremental portion (i.e. 8.5% or 16.5%, depending on the entity’s R&D intensity) is accounted for using the principles of AASB 120.

Proponents of the hybrid approach view the portion of the R&DTI that equates to the corporate tax rate as more akin to a tax deduction as, should the entity choose not to claim the R&DTI, the entity will still be entitled to a tax deduction for the eligible R&D spend at the relevant corporate tax rate. The benefit over and above this is considered to be akin to a government grant, being the benefit that would otherwise not be received had the entity not claimed the R&D offset under the scheme.

Conclusion

The changes to the R&D tax offset rules are not expected to change the way they are dealt with from an accounting perspective. However, this is a good time for entities that undertake R&D activities to review their R&D policies and processes to ensure they have every chance of qualifying for the new and improved R&DTI. At the same time, entities should pay attention to the accounting implications which, quite often, are not considered properly and can be material. It is important that R&D tax offsets are appropriately and transparently dealt with in the financial statements.