The pandemic and rolling lockdowns has forced many Australians to rethink their 2021 holiday plans. While a trip away may bring short term enjoyment, investing in your superannuation through concessional contributions may present long-term benefits.

What are concessional contributions?

Concessional contributions are before tax contributions to your superannuation fund that enable a tax deduction to be claimed. They can be made by your employer (i.e. superannuation guarantee contributions, or voluntary salary sacrificed contributions), or by way of a personal contribution. A personal concessional contribution provides a tax benefit equal to the difference between an individual’s marginal rate of tax and the superannuation tax rate of 15%.

The general concessional contributions cap during the years 1 July 2017 to 30 June 2021 was set at a maximum of $25,000 per annum. This increased to $27,500 from 1 July 2021. Employer superannuation guarantee contribution and salary sacrificed amounts count towards the concessional contribution cap.

From 1 July 2018 the concept of carrying forward any unused concessional contributions cap was introduced. Meaning it is now possible to make additional concessional contributions, above the general concessional contribution cap, in a financial year by utilising unused cap amounts from prior years. Previously, if the concessional contribution cap was not fully utilised each financial year, it was permanently lost.

Utilising unused concessional caps

The unused cap is available providing the following conditions are met:

- Your total super balance at the end of 30 June of the previous financial year is less than $500,000; and

- Concessional contributions are made in a financial year that exceed the general concessional contributions cap (i.e. concessional contributions must be over $27,500 for the 2021-2022 financial year). If concessional contributions of less than the general cap are made in a financial year the contributions will count towards the current year contribution cap and the carry forward unused cap will not be affected.

Additionally, the unused amounts can be carried for up to five financial years and if utilised are applied on a first-in-first-out (FIFO) basis. Therefore, the unused cap carried forward from the 2018-2019 financial year will expire if not used by the end of the 2023-2024 financial year.

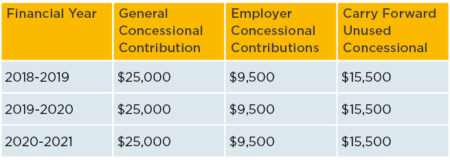

Example 1: Utilising the unused cap

Bob earns $100,000 plus superannuation guarantee of $9,500 per annum and has made no additional personal or voluntary salary sacrificed concessional contributions since 1 July 2018. Bob’s total super balance is $480,000 as at 30 June 2021. Bob’s carry forward unused concessional contributions cap is $46,500 as at 30 June 2021, illustrated as follows:

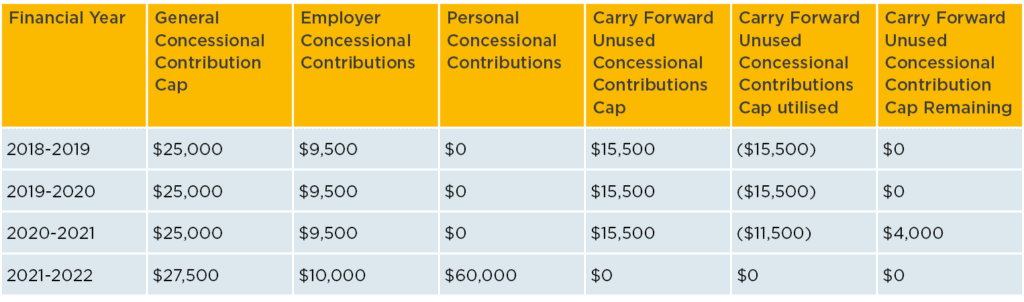

In August 2021, Bob inherits $60,000 cash and would like to put the money away for his retirement so decides to access the carry forward unused concessional contributions cap by contributing the whole amount to his super fund. The 2021-2022 personal concessional contributions will result in the following:

As one of the requirements to access the unused caps is to fully utilise the current year general concessional contribution cap, $17,500 of the $60,000 contribution counts towards the 2021-2022 concessional contribution cap. Therefore, leaving $42,500 to offset against the prior year unused caps.

Bob’s remaining carry forward concessional contribution cap is $4,000, and as any unused amounts are utilised on a FIFO basis is attributable to the 2020-2021 financial year. He has until the end of the 2025-2026 financial year before this unused cap expires.

The net tax benefit to Bob is $9,300; being a tax saving in his personal tax return of $18,300 less tax payable in his super fund of $9,000.

Utilising Single Touch Payroll

Assessment of an individual’s carry forward unused concessional contribution amount is assisted by the new Single Touch Payroll system (STP). It is the system responsible for individuals no longer receiving a Group Certificate/PAYG Payment Summaries from their employer at year end. Essentially weekly/fortnightly or monthly payroll data is transmitted by employers to the ATO each time a payroll period is paid. One of the ancillary benefits of STP is the system allows tax agents to gain access to the carry forward unused cap amounts of their clients. For those self-employed and not currently using STP, there is a need for more records to be obtained to establish what carry forward unused concessional contribution caps are available.

Division 293 tax when utilising unused caps

Division 293 tax is an additional 15% tax on concessional contributions for individuals who’s Division 293 income exceeds $250,000. Utilising the carry forward unused caps will add to your division 293 income and may result in Division 293 tax being payable, and thus reducing the overall benefit.

Example 2: Division 293 tax when utilising unused caps

Jane earns a salary of $300,000 per annum and meets the requirements to access the carry forward unused concessional contribution caps. Jane has total unused caps of $30,000 and utilises this in the 2021-2022 financial year, which provides a net tax benefit of $9,600. As a result, the ATO will issue a Division 293 tax assessment for the amount of $4,500, thereby reducing the net tax benefit for Jane to $5,100.

Key considerations

- As the tax benefit is equal to an individual’s marginal rate of tax less the superannuation tax rate, an individual’s taxable income will determine the underlying benefit of utilising the unused caps.

- Although there can be a significant tax benefit from accessing the unused caps, it is important to understand that whilst your super is in accumulation phase the contributions must remain in the superannuation environment until such time as you can legally access your superannuation benefits. This is essential to understand for personal budgeting and cashflow purposes as any contributions made are then locked in the superannuation system until such time you meet a condition of release of your benefits (i.e. attaining retirement age, commencement of a pension).

- If you exceed both the general concessional and carry forward unused caps additional tax may be payable, therefore it is imperative that an accurate calculation of available unused caps be prepared prior to making any concessional contributions.

Please contact us to assist with this modelling to ensure any strategy in this area is customised to your particular tax circumstances.

The information contained on this website has been provided as general advice only. The contents have been prepared without taking account of your personal objectives, financial situation or needs. You should, before you make any decision regarding any information, strategies or products mentioned on this website, consult your own financial adviser to consider whether that is appropriate having regard to your own objectives, financial situation and needs.